Swiggy IPO: Things to Know Before Subscribing

Executive Summary:

Swiggy, established in 2014 in Bangalore, has emerged as a leading player in India’s food delivery landscape. It made history by becoming the quickest Indian startup to attain unicorn status, showcasing its immense growth potential. Operating across 500+ cities nationwide,

Swiggy has collaborations with a vast network of over 150,000 restaurant partners, offering customers an extensive array of culinary choices. To facilitate seamless and prompt deliveries, Swiggy boasts a sizable fleet of more than 260,000 delivery personnel, underscoring its commitment to efficiency and customer satisfaction.

In this note, we take a quick look at the key highlights of the offering along with a brief overview of the food delivery and quick commerce industry outlook and deep dive into the company’s financials in comparison to its listed peers.

| Key Things to Know | |

| IPO Date | 6th Nov 2024 – 8th Nov 2024 |

| Price Band | Rs 371-390 per share |

| Total Issue Size | Rs 11,327.43 Cr crores |

| Fresh Issue | Rs 4,499 crores |

| Offer for Sale | Rs 6,828.43 crores |

| Post Issue M-cap | Rs 1,07,000 crores |

| QIB quota | 75% |

| Retail quota | 10% |

| NII(HNI) quota | 15% |

Before we delve deeper, let’s look at the valuation of the IPO.

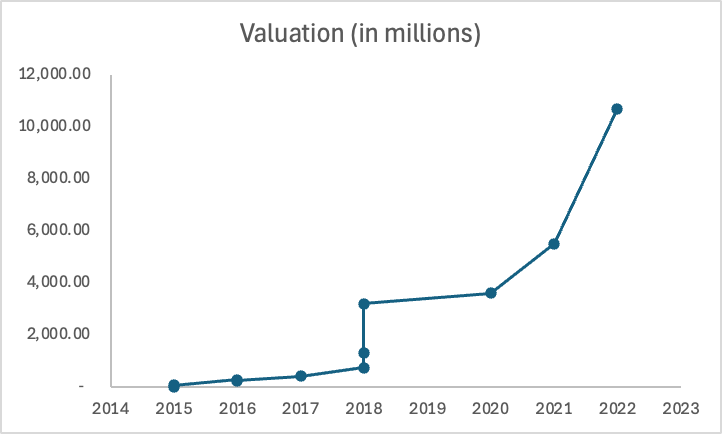

Valuation:

Launched IPO at a slightly higher valuation of $11.3bn ~5% premium to its last funding round in September

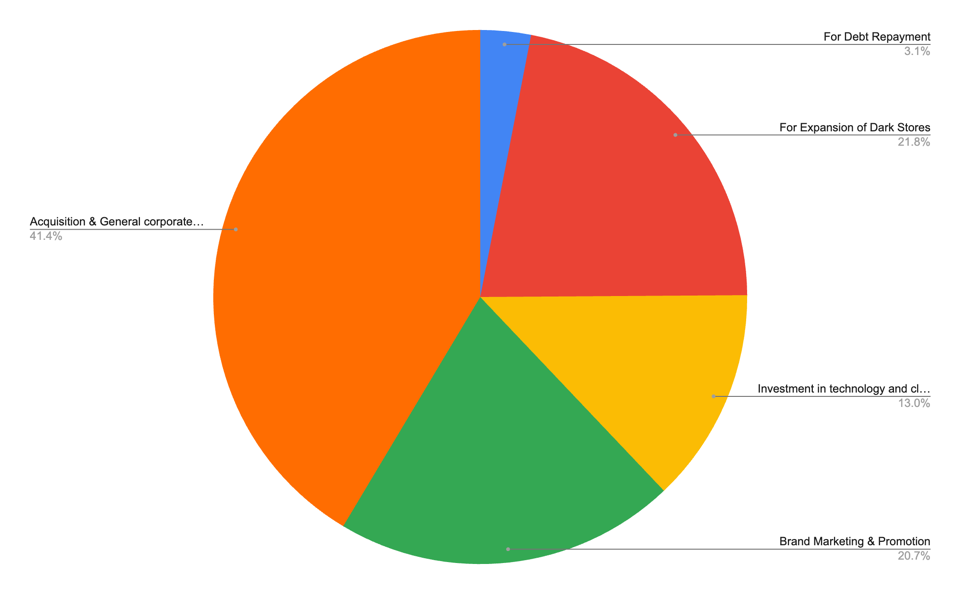

Where will the money be utilized?

Industry Overview & Outlook:

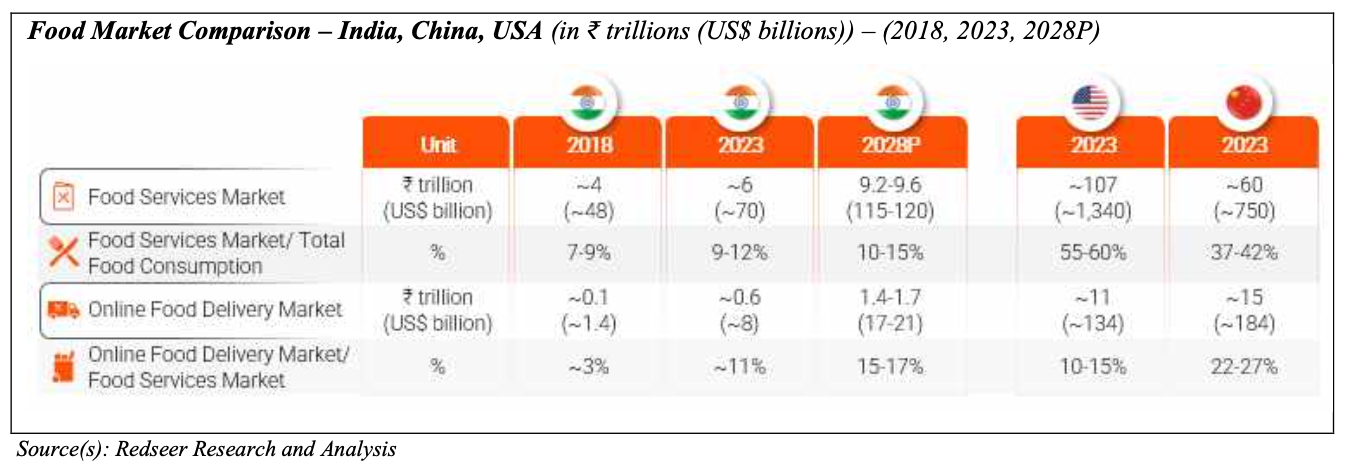

The Indian food services market comprises online Food Delivery and Out-of-home Consumption which was ₹5,600 billion (US$70 billion) as of 2023. The online Food Delivery market is the fastest growing segment within the food services market and is expected to grow at 17-22% between 2023 and 2028. In the Out-of-home Consumption market, the organised segment and the online dining out segment is expected to grow at 15-18% and 46-53% respectively between 2023 and 2028. Both online Food Delivery and Out-of-home Consumption markets are growing on the back of rapid increase in share of organised restaurant supply unlocking demand in the Indian market.

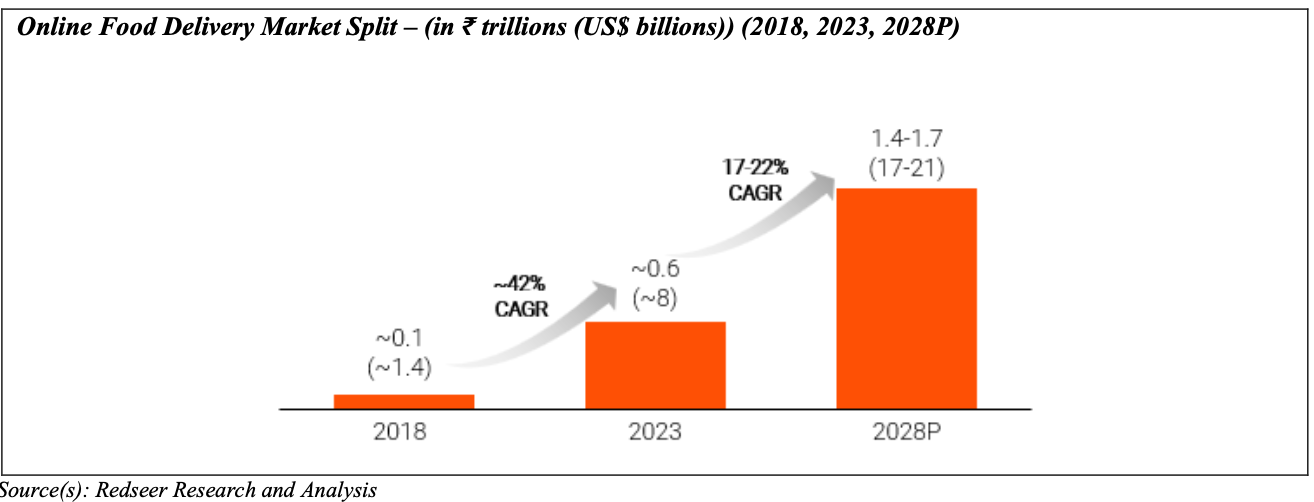

The online Food Delivery market in India grew from ₹112 billion (US$1.4 billion) in 2018 to ₹640 billion (US$8 billion) in 2023 and is expected to become a ₹1400-1700 billion (US$17-21 billion) market by 2028P, growing at a CAGR of 17-22%. Of the total market in 2023, the share of top 60 cities (metro and Tier 1) is 75-80% which shows the large untapped potential beyond these cities which will drive growth as penetration of online Food Delivery increases. Growing availability of organised restaurant supply and increased online penetration is expected to drive growth in online Food Delivery market beyond the top 60 cities.

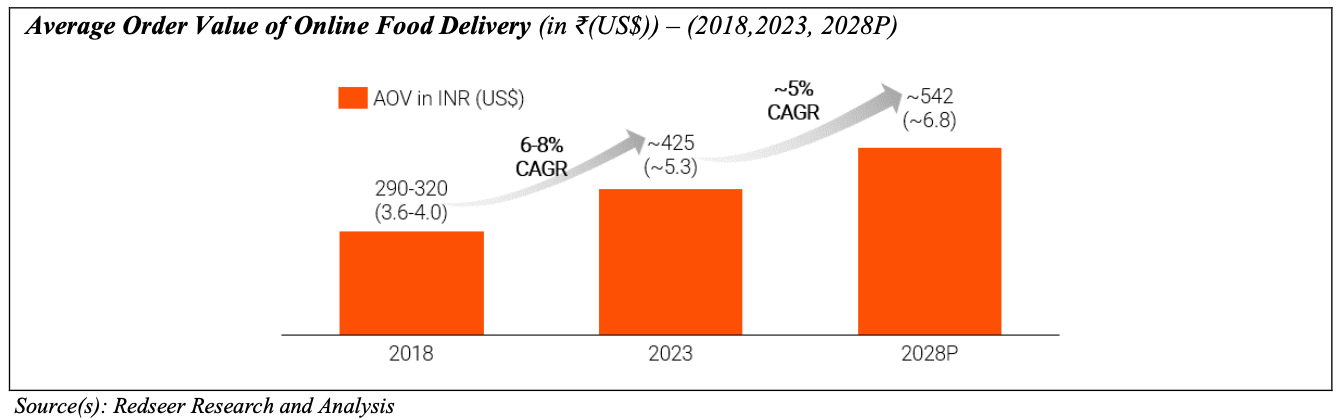

The Average Order Value (“AOV”) (average monetary value of a single order pre-discount and including taxes, customer delivery charges but excluding tips) for the industry has also climbed from approximately ₹290-320 (US$3.6-4.0) in 2018 to approximately ₹425 (US$5.3) in 2023. Apart from inflation, this surge is attributed to supply-side innovations like higher presence of premium restaurants, more premium dishes and on the demand side this is caused by increasing disposable incomes, increased appetite for experimentation and a change in the consumer base with a larger proportion of families opting for online food ordering. Globally as well, PPP-adjusted AOVs are significantly higher at ₹600-650 (US$7.5-8.1) and ₹750-800 (US$9.4-10.0) in the USA and UK, respectively, signalling clear headroom to grow in the future.

Online penetration in the retail market is growing on the back of rising consumer demand and need for convenience through doorstep deliveries. Among the fastest growing online categories are food at-home (grocery), personal care products, fashion, electronics devices and appliances and pharmaceuticals, growing at CAGRs of approximately 46%, 40%, 34%, 29% and 24% respectively between 2018 and 2023. Apart from supply-side factors like the large untapped and unorganised market, improved brand reach and visibility, increasing store density and revenue enhancement, there are several consumer-led factors like consistent demand and need for improved access and availability which makes these categories particularly appropriate for online growth.

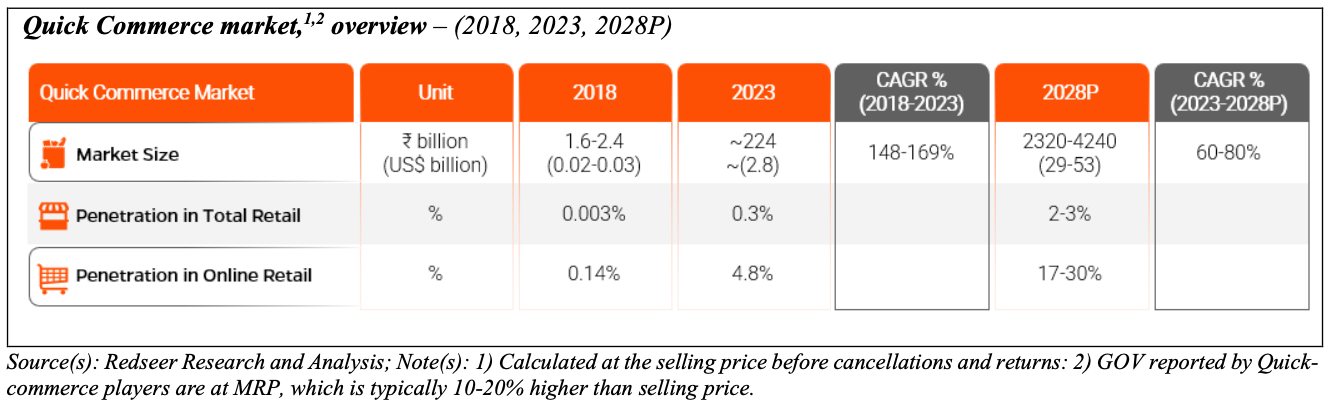

Quick Commerce has largely been a successful mode in terms of profitability in India due to its high density micro-markets and low penetration of organised brick and mortar (B&M) grocery. The share of the Quick Commerce market in online retail has increased rapidly from approximately 0.14% in 2018 to 4.8% in 2023 and with fast-paced growth of 60-80% expected annually till 2028, it is expected to reach 17-30% penetration in online retail resulting in a Quick Commerce market size of ₹2320-4240 billion (US$ 29-53 billion).

Threats and Challenges to Hyperlocal Players

While the Hyperlocal Industry in India is expected to see significant growth as outlined in the previous sections, players may face several threats and challenges that could impede their growth trajectory and stability as outlined below:

• Economic and Inflationary Pressures- Economic downturns and rising inflation could limit disposable income, impacting some discretionary spends on Hyperlocal Platforms.

• Regulatory and Policy Risks- Stricter safety regulations and changes in gig economy laws could increase operational costs for Hyperlocal Platforms which may get passed on to end consumers, potentially reducing their rate of adoption

• Competition: Intensified competition from existing players, new entrants and companies from other sectors leveraging their existing capabilities for certain hyperlocal services like Quick Commerce, can raise competitive intensity which can have implications for change in business economics, scope and scale of categories and geographies catered to by the model, and market positions of players.

• Rise of Other Models: Select large businesses can develop their own apps and delivery services to bypass third-party platforms however has seen limited adoption currently. Successful execution of this trend could reduce the volume of orders on these platforms as customers might prefer ordering directly from these businesses. Emergence of models like Open Network for Digital Commerce (ONDC) are an example of this trend by allowing businesses to connect directly with consumers, bypassing third-party intermediaries.

• Logistics Complexity: Efficiently meeting demand across diverse locations can be challenging due to external factors such as traffic, weather conditions which may impact customer experience. Additionally, as these platforms grow, these platforms need to continuously recruit, train, and retain delivery partners and customer service representatives

• Ability to Add New Categories Profitably: Certain segments like Quick Commerce are rapidly evolving with multiple new categories being added. The evolution of these new categories is yet to be proven in terms of operational complexity and profitability at scale

Peer Comparison:

| Valuation | Sales | Food Delivery | Quick Commerce | |||||

| GOV CAGR | AOV | EBITDA Margins% | No. of Dark Stores | AOV | EBITDA Margins% | |||

| Swiggy | ₹1.07 lakh crore | ₹ 11,247 crore | 15.50% | ₹436 | 0.80% | 557 | ~₹350 | -11.7 |

| Zomato | ₹2.14 lakh crore | ₹ 12,114 crore | 23% | ₹425 | 3.60% | 639 | ~₹600 | -0.1 |

- Zomato is the listed peer which can be used for relative valuation, we believe looking at operational parameters that swiggy is fairly valued and the valuation gap between two is justified at the current stage.

- Zomato is valued at $ 26.5 bn and Swiggy is asking for a valuation of $ 11.3 bn. Swiggy lags in EBITDA margins for food delivery business and Average order value for quick commerce business.

- In food delivery, the market share is 45-55% in terms of revenue and 40-60% from no. of orders for Swiggy-Zomato respectively.

- Zomato’s quick commerce app currently beats Swiggy’s with respect to monthly transacting users, average order value, Efficiency and Take-Rate from Brands.

- One clear advantage Zomato has against Swiggy is Hyperpure, Hyperpure has demonstrated impressive growth metrics, with revenues doubling year-on-year. For Q3 FY24 alone, Hyperpure reported a revenue of ₹859 crore.

Our Take: Almost 50% valuation compared to Zomato gives some comfort although it should not be considered as an arbitrage in valuation

If Swiggy’s EBITDA catches up to 3-4% in the food delivery business, which is currently at 1% and Average Order Value (AOV) improves to Rs. 550-600 levels in quick commerce with higher non-grocery share, we can see bridging in the valuation gap. Although, this should not be expected in near

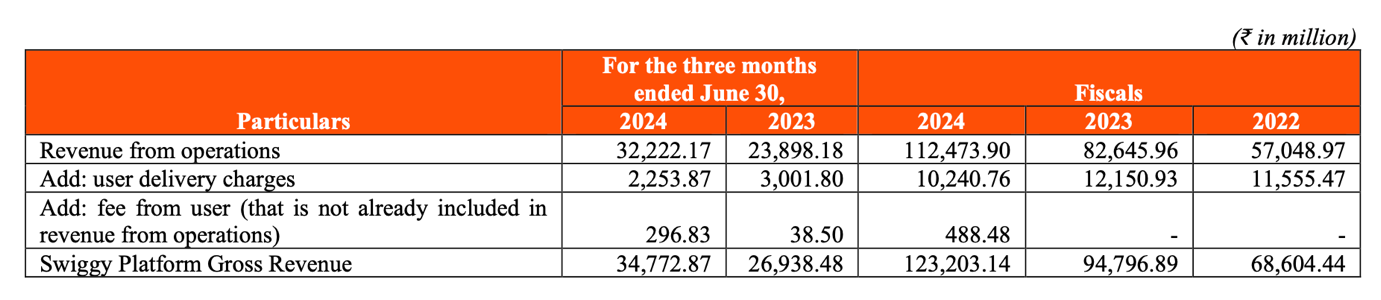

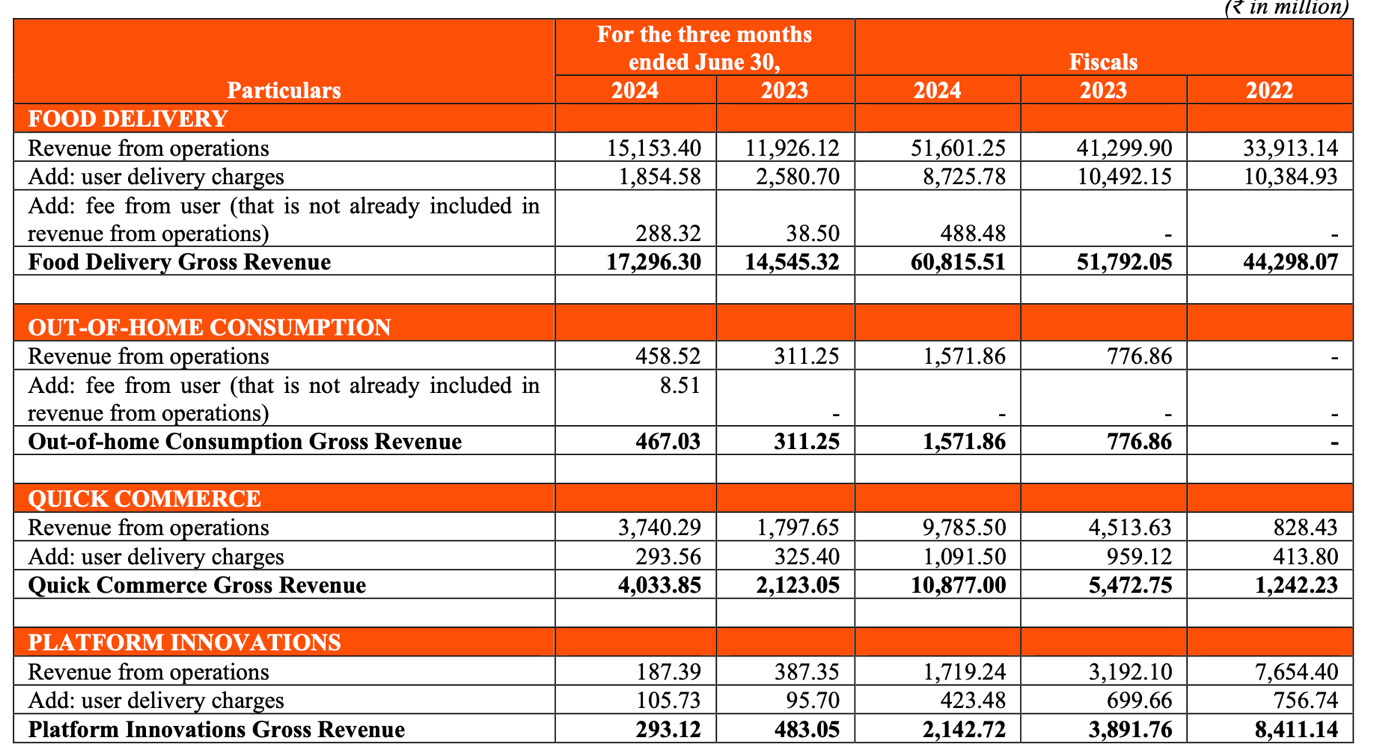

KeyFinancials

Disclaimer

The stocks mentioned in this article are not recommendations. Please conduct your own research and due diligence before investing. Investment in securities market are subject to market risks, read all the related documents carefully before investing. Please read the Risk Disclosure documents carefully before investing in Equity Shares, Derivatives, Mutual fund, and/or other instruments traded on the Stock Exchanges. As investments are subject to market risks and price fluctuation risk, there is no assurance or guarantee that the investment objectives shall be achieved. Lemonn (Formerly known as NU Investors Technologies Pvt. Ltd) do not guarantee any assured returns on any investments. Past performance of securities/instruments is not indicative of their future performance.