NTPC Green Energy Limited – IPO Highlights

Introduction

NTPC Green Energy, a subsidiary of India’s largest power generation company NTPC Limited, was established in 2022 to spearhead the state-backed entity’s renewable energy initiatives. This strategic move aligns with India’s national target of installing 500 GW of clean energy capacity by 2030, positioning NTPC Green Energy as a key player in the country’s sustainable future.

Operational Capacity: 3,320 MW (3,220 MW solar, 100 MW wind)

Project Pipeline: 13,576 MW (contracted and awarded), 9,175 MW (in development)

Diverse Portfolio: Assets spread across six Indian states

Strategic Backing: Supported by NTPC Limited, ensuring financial stability and industry expertise

In this note, we take a quick look at the key highlights of the offering along with a brief overview of the Green energy industry outlook and deep dive into the company’s financials in comparison to its listed peers.

| Key Things to Know | |

| IPO Date | 19th Nov 2024 – 22nd Nov 2024 |

| Price Band | Rs 102-108 per share |

| Total Issue Size | Rs 10,000 crores |

| Fresh Issue | Rs 10,000 crores |

| Offer for Sale | Rs 0 crores |

| Post Issue M-cap | Rs. 86,500 – 91,000 crores |

| QIB quota | 75% |

| Retail quota | 10% |

| NII(HNI) quota | 15% |

Key Highlights:

1. Strong parentage: The company is a wholly owned subsidiary of NTPC Ltd, a ‘Maharatna’ central public service enterprise, which contributes ~17% to India’s total installed capacity and ~24% to the total power generated in India as of Sep’24. NGEL benefits from the support, vision, resources and experience of the NTPC group which is currently looking to expand its non-fossil-based capacity to 45-50% of its portfolio which will include 60 GW renewable energy capacity by CY32. The company believes it can use the brand recall and long-term experience of dealing with state DISCOMs of NTPC Ltd to grow its portfolio and business in India.

2. Robust product portfolio with diversification across geographies and offtakes: NGEL has a large portfolio of utility-scale solar and wind energy projects coupled with projects for PSUs and Indian corporates. As of Sep’24, the company had 17 off-takers across 41 solar and 1 wind projects. The total portfolio as of Sep’24, consists of 26,071 MW including 3,320 MW of operating projects; 13,576 MW of contracted & awarded projects and 9,175 MW of capacity under pipeline. NGEL’s portfolio is spread out across Rajasthan, Gujarat, Tamil Nadu, Andhra Pradesh, Madhya Pradesh and Uttar Pradesh which helps in mitigating risk of location specific generation variability.

3. Experience in renewable energy project execution: The company along with the NTPC Group have a strong track record of developing, constructing and operating renewable power projects, driven by experienced in-house management and procurement teams. NGEL’s in-house team works with third-party aggregators, developers and EPC contractors to manage the land acquisition process. As of Sep’24, the company owns ~8,900 acres of freehold land and ~45,700 acres of leasehold land. Further, the company aims to leverage NTPC Group’s economies of scale to negotiate and reduce the cost of components, equipment and materials for its solar and wind projects from domestic and foreign original equipment manufacturers and suppliers.

4. Access to low cost of capital: The company’s focus on maintaining high capacity utilization, operational efficiencies, low operating costs along with the strong parentage and diversified portfolio helps it to maintain healthy coverage ratios. Further, leveraging NTPC group’s high credit rating and strong balance sheet provides access to low cost of capital. Before we delve deeper, let’s look at the valuation of the IPO.

Valuation:

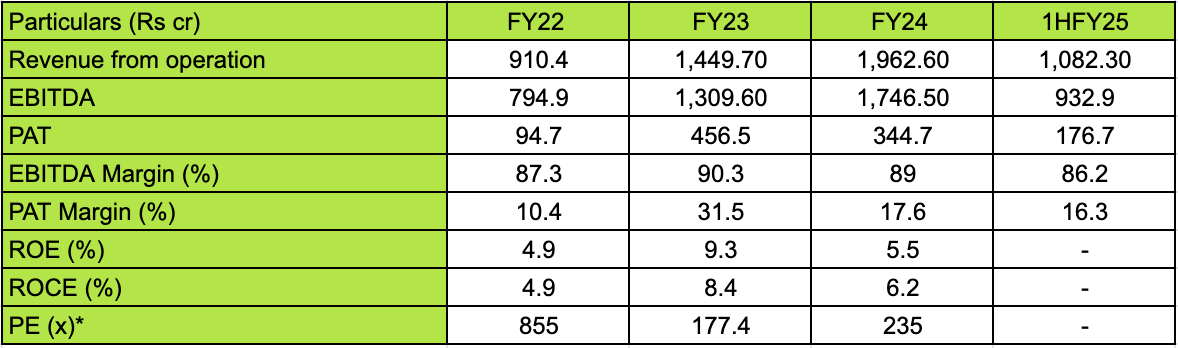

At the upper price band of Rs 108, NGEL is valued at FY24 EV/EBITDA of 53.4x on post issue capital. The company will increase its operational capacity to 6/11/19 GW by FY25E/FY26E/FY27E respectively from 3.3 GW as of Sep’24.

Basis on our calculation, at upper price band, the issue is priced at FY25E/FY26E/FY27E EV/EBITDA multiple of 35.3x/18.3x/10.1x and EV/MW of Rs 16.8 cr./9.0 cr./5.1 cr. respectively. The company has exponential growth potential in medium term with its Revenue/EBITDA/PAT expected to grow at a CAGR of 79.0%/117.2%/123.8% to Rs 11,250 cr./9,563 cr./1,980 cr. respectively over FY24-27E period.

Where will the money be utilized?

- Investment in our wholly owned Subsidiary, NTPC Renewable Energy Limited (NREL) for repayment/ prepayment, in full or in part of certain outstanding borrowings availed by NREL– Rs. 7500 crores

- General Corporate Purpose and to be decided – Rs. 2500 crores

Industry Overview & Outlook:

- India’s Energy Demand stood at 1,627 BU in FY24 and is projected to grow at a CAGR of ~5.5% between FY24-FY29P to reach 2,170 BU. The growth would be driven by infrastructure-linked capex, strong economic fundamentals along with expansion of the power footprint via strengthening of T&D infrastructure, coupled with major reforms initiated by the Government of India for improving the overall health of the power sector, particularly that of state distribution utilities.

- India’s Renewable Energy Capacity has increased from 63 GW as of Mar’12 to 201 GW as of Sep’24 driven by various central and state government schemes. As of Sep’24, renewable energy constitutes ~44% of the total installed power capacity in India, however due to lower capacity utilization renewable energy contributes only ~23% to the energy generated.

- All India Installed Capacity is expected to grow from 442 GW in FY24 to 667 GW in FY29P, largely contributed by renewable energy additions (+187 GW). Addition of incremental renewable capacity is likely to be driven by various government initiatives, favorable policies, competitive tariffs, innovative tenders, development of solar parks and green energy corridors, etc. Further, Renewable energy capacity is estimated to account for ~50% of India’s total installed capacity of 660-670 GW by FY29.

- The Solar Energy Sector in India is growing exponentially, backed by robust government support demonstrated through an aggressive tendering strategy. Some of the key catalysts include technological advancements, affordable financing, supportive policies, thrust on go-green initiatives/sustainability targets, cost optimization due to increased grid electricity tariffs, subsidy initiative (specially in rooftop solar) and various incentives such as ISTS charge waiver. The industry is projected to increase installed capacity by ~174 GW between FY25-FY29P driven by various government schemes and corporates focusing on ESG factors.

- The Wind Energy Sector in India is projected to add ~40 GW of installed capacity between FY25-FY29P driven by pipeline buildup under existing schemes and new tendering schemes, improvement in technology, thrust on green hydrogen, renewable generation obligation and mixed resource models.

Peer Comparison

| Particulars (Rs cr) | NTPC Green Energy Ltd | Adani Green Energy Ltd | ACME Solar Holdings Ltd |

| Operational Capacity (MW) | 2,925.00 | 10,934.00 | 1,340.00 |

| CMP | 108 | 1,469.00 | 255.2 |

| Sales | 1,962.60 | 9,220.00 | 1,319.30 |

| EBITDA | 1,746.50 | 7,318.00 | 1,089.10 |

| Net Profit | 344.7 | 1,260.00 | -50.9 |

| Mkt Cap. | 91,000.00 | 2,32,734.0 | 15,438.80 |

| Enterprise Value | 93,324.60 | 2,94,292.0 | 25,367.00 |

| EBITDA Margin (%) | 89 | 79.4 | 82.6 |

| Net Margin (%) | 17.6 | 13.7 | – |

| PE (x) | 264 | 184.7 | – |

| EV/EBITDA (x) | 53.4 | 40.2 | 23.3 |

| RoE (%) | 5.5 | 17.1 | 26.9 |

| RoCE (%) | 6.2 | 9.8 | 8.6 |

| EV/Sales | 47.6 | 31.9 | 19.2 |

| EV/MW (FY24) | 31.9 | 26.9 | 18.9 |

| EV/MW (FY25E) | 16.8 | – | – |

| EV/MW (FY26E) | 9 | – | – |

| EV/MW (FY27E) | 5.1 | – | – |

Our Take:

- In terms of valuation, the IPO is priced aggressively at a P/E ratio of 264x as of FY 2024, which is significantly higher than its peers

- The aggressive valuation suggests that the IPO may be suited for only investors with a high-risk appetite.

- The company has commendable growth potential in a growing sector, its high valuation could pose risks in the short term.

Disclaimer

The stocks mentioned in this article are not recommendations. Please conduct your own research and due diligence before investing. Investment in securities market are subject to market risks, read all the related documents carefully before investing. Please read the Risk Disclosure documents carefully before investing in Equity Shares, Derivatives, Mutual fund, and/or other instruments traded on the Stock Exchanges. As investments are subject to market risks and price fluctuation risk, there is no assurance or guarantee that the investment objectives shall be achieved. Lemonn (Formerly known as NU Investors Technologies Pvt. Ltd) do not guarantee any assured returns on any investments. Past performance of securities/instruments is not indicative of their future performance.