Mobikwik IPO Highlights

Introduction

In this note, we take a quick look at the key highlights of the offering along with a brief overview of the digital payments industry and industry outlook and deep dive into the company’s financials in comparison to its listed peers.

| Key Things to Know | |

| IPO Date | 11th Dec – 13th Dec 2024 |

| Price Band | Rs 265-279 per share |

| Total Issue Size | Rs 572 crores |

| Fresh Issue | Rs 572 crores |

| Offer for Sale | Rs 0 crores |

| Post Issue M-cap | Rs. 2295 crores |

| QIB quota | 75% |

| Retail quota | 10% |

| NII(HNI) quota | 15% |

OMSL is fundamentally a platform business, operating a two-sided payments network that connects consumers and merchants. As of June 30, 2024, the company has amassed 161.03 million registered users and empowered 4.26 million merchants to seamlessly make and accept payments both online and offline. Its platform becomes increasingly valuable to both new and existing users by continuously adding innovative products in digital credit, investments, and insurance. By expanding its offerings across these verticals, OMSL is not only enhancing its appeal to consumers but also driving profitability and shareholder value. This strategy has translated into a profit of ₹14.08 crore for the year ending March 31, 2024. The company is steadfast in its mission to harness technology as a catalyst for advancing financial inclusion among India’s underserved population.

OMSL’s growth is fueled by frugal, digital-first innovations, as demonstrated by its robust portfolio of scalable products. The company maintains one of the lowest employee cost-to-revenue ratios among digital financial platforms, underscoring its operational efficiency (Source: RedSeer Report). Between Fiscal 2022 and Fiscal 2024, OMSL achieved remarkable growth, with Payment GMV increasing at a CAGR of 45.88% and Mobikwik ZIP GMV (disbursements) expanding at an impressive CAGR of 112.16%. Its offerings span payments, consumer credit, investments, and insurance, including the introduction of co-branded credit cards backed by fixed deposits, catering to diverse customer needs.

The Indian financial services market remains vastly underpenetrated across key segments such as lending, insurance, and mutual funds, according to the RedSeer Report. This presents a tremendous opportunity for a technology-driven company like Mobikwik to capture a significant share of this market. Insights gathered from meticulous market analysis highlight that consumers, particularly in middle- and low-income segments, face substantial barriers to accessing financial services. Leveraging this data, OMSL has identified strategic product opportunities that position it to tap into these underserved and untapped markets, driving both growth and inclusion.

Revenue Breakup

| Particulars | For 3 months ended June 30, 2024 (%) | 2024 (%) | 2023 (%) | 2022 (%) |

| Payment Services | 171.54 (50.12%) | 317.12 (36.24%) | 254.45 (47.17%) | 428.91 (81.45%) |

| Financial Services | 170.73 (49.88%) | 557.88 (63.76%) | 285.02 (52.83%) | 97.657 (18.55%) |

| Revenue from Operations | 342.27 (100.00%) | 875.00 (100.00%) | 539.47 (100.00%) | 526.57 (100.00%) |

Before we delve deeper, let’s look at the valuation of the IPO.

Valuation:

- The IPO at highest price band is attractively priced at 2.6x of FY24 revenue.

- The issue is priced at a P/BV of 10.06 based on its NAV of Rs. 27.74 as of June 30, 2024, and at a P/BV of 2.97 based on its post-IPO NAV of Rs. 94.05 (at the upper cap).

Where will the money be utilized?

| Objects of the Issue | Amount (₹ Cr) |

| Funding organic growth in the financial services business | 150 |

| Funding organic growth in the payment services business | 135 |

| Research and development in data, ML, AI, and product technology | 107 |

| Capital expenditure for the payment devices business | 70.29 |

| General Corporate Purposes & Others | 109.71 |

| Total | 572 |

Industry Overview

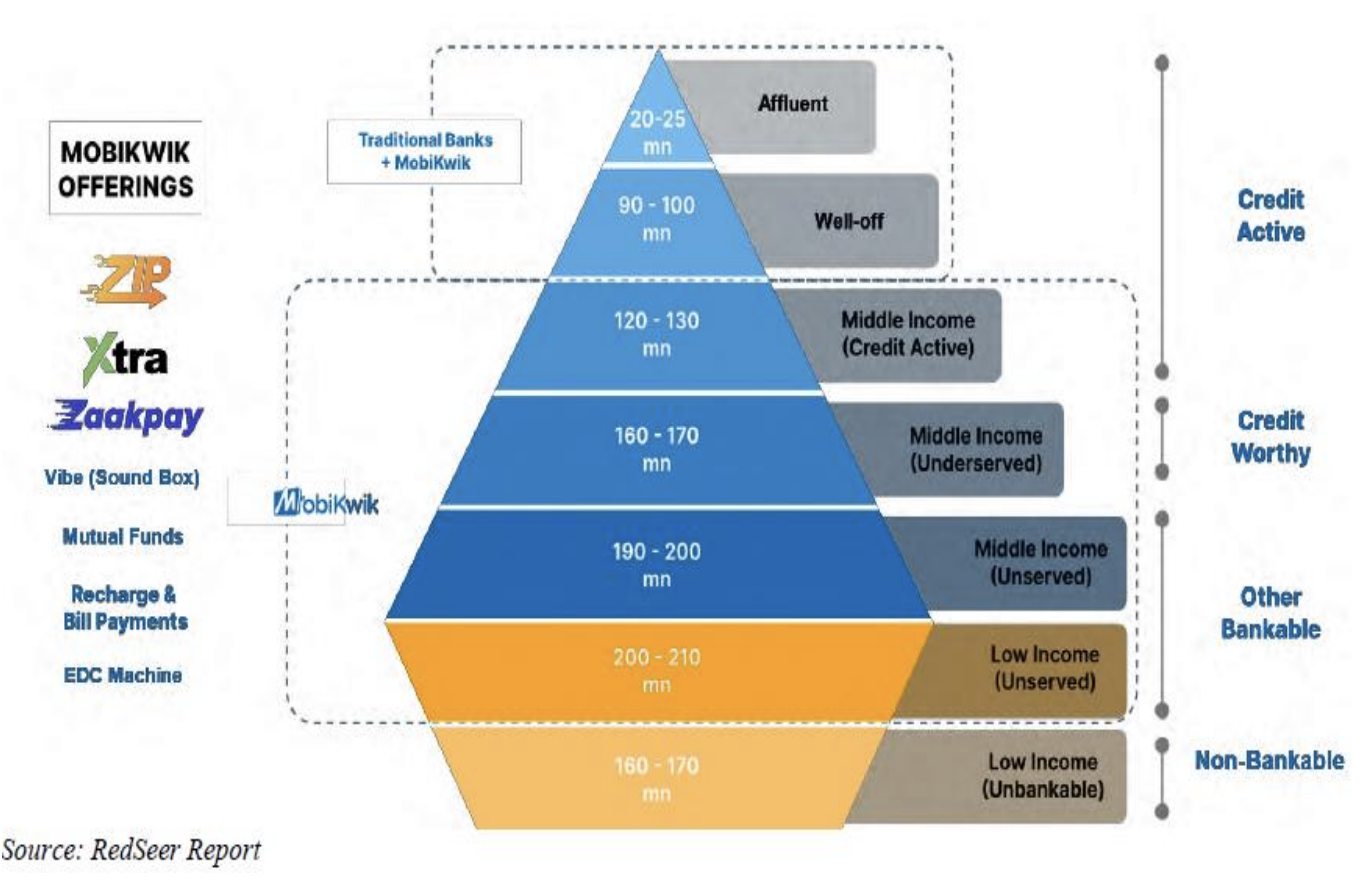

According to the RedSeer Report, India’s financial services sector remains highly underpenetrated across critical segments such as lending, insurance, and mutual funds. This underpenetration presents a vast opportunity for technology-driven companies like One Mobikwik Systems Ltd.

The company strategically focuses on serving the “bankable middle-India” population, which is often overlooked by traditional market players. Currently, these players cater primarily to the 20-25 million affluent individuals and 90-100 million well-off individuals in the country. However, there is an untapped market of over 500 million individuals in the middle-India segment who are underserved.

Within this group, 120-130 million individuals are already credit active, highlighting an immediate opportunity to expand financial products. Additionally, more than 400 million consumers currently lack access to credit but require financial services. By leveraging its extensive payments data, Mobikwik can offer smaller loans to these individuals, helping them build credit histories and enabling their inclusion into the formal financial system. This approach positions the company as a key enabler of financial inclusion across the country.

The company’s target market segments in India present significant GMV growth potential as reflected in the projected growth of such industries over the next few years. The overall market is poised to grow at the rate of 21% CAGR from FY2023 to FY 2028.

The company operates in an addressable market estimated at approximately USD 5.3 billion (₹424 billion), which is expected to grow significantly to USD 16-18 billion (₹1.3 trillion – ₹1.4 trillion) by FY2028.

Key Financials

| KPIs | June 30, 2024 | 2024 | 2023 | 2022 |

| Merchants (Million) | 4.26 | 4.06 | 3.74 | 3.6 |

| Platform Spend GMV (₹ Cr.) | 28,578 | 47,678 | 26,235 | 23,632 |

| Registered Users (Million) | 161 | 156 | 140 | 124 |

| Digital Credit GMV (₹ Cr.) | 2,347 | 9,093 | 5,115 | 1,512 |

| Payment GMV (₹ Cr.) | 25,080 | 38,195 | 20,725 | 17,947 |

| Payment Gateway GMV (Disbursements) (₹ Cr.) | 2,028 | 3,412 | 1,407 | 4,336 |

| MobiKwik ZIP GMV (₹ Cr.) | 1,470 | 6,070 | 4,103 | 1,349 |

| ZIP EMI GMV (Disbursements) (₹ Cr.) | 876 | 3,023 | 1,012 | 164 |

| New Registered Users (Million) | 5.2 | 16.0 | 16.3 | 22.2 |

| Customer Acquisition Cost (₹) | 34 | 33 | 20 | 18 |

| Activated – MobiKwik Zip Users (Million) | 6.2 | 5.9 | 4.1 | 2.4 |

| Activated – MobiKwik Zip EMI Users (Million) | 1.0 | 0.9 | 0.5 | 0.3 |

| Repeat MobiKwik Zip Users (%) | 0.9 | 0.9 | 0.9 | 0.8 |

| Credit – Partner AUM (₹ Cr.) | 2,495 | 2,384 | 718 | 177 |

| Wealth – AUA (₹ Cr.) | 6,693 | 5,981 | 817 | 324 |

| Lending Related Expenses (%) | 4% | 3% | 3% | 7% |

| Gross Margin – Financial Services (%) | 44% | 46% | 38% | -11% |

| Gross Margin – Payment Services (%) | 16% | 19% | 18% | 32% |

| Overall Contribution Margin (%) | 31% | 37% | 31% | 26% |

| Offline Merchants (Million) | 413% | 393% | 364% | 352% |

| Online Merchants (Million) | 13% | 13% | 9% | 8% |

| Employee Cost (%) | 11% | 13% | 18% | 20% |

| Billers (No’s) | 463 | 463 | 438 | 438 |

| Digital Credit Active Users (Million) | 7 | 7 | 5 | 3 |

| MobiKwik ZIP Ticket Size (₹) | 5,594 | 6,582 | 6,334 | 3,349 |

| MobiKwik ZIP Pre-approved Users (Million) | 34 | 34 | 32 | 30 |

| MobiKwik ZIP Active Merchants (No’s) | 18,408 | 32,898 | 31,598 | 20,671 |

| Payments Take Rate (%) | 0.7% | 0.8% | 1.2% | 2.4% |

| Financial Services Take Rate (%) | 7.3% | 6.1% | 5.6% | 6.5% |

| ZIP EMI Ticket Size (₹) | 10,000 to 2,00,000 | |||

Peer Comparison

| Company Name | Face Value (₹) | CMP as on Dec 3, 2024 (₹) | Total Income (₹ Cr) | EPS (₹) | P/E | MCap/Revenue | RONW | |

| Basic | Diluted | |||||||

| Domestic Peers | ||||||||

| One MobiKwik Systems | 2 | NA | 890.32 | 2.46 | 2.38 | [ • ] | [ • ] | 8.66 |

| One 97 Communications | 1 | 902.6 | 10,524.70 | -22.33 | -22.33 | NA | 5.44 | -10.7 |

| Global Peers | ||||||||

| Affirm Holdings, Inc@ | 0.0008 | 5,660.80 | 18,583.99 | -133.6 | -133.6 | NA | 9.47 | -18.95 |

| PayPal Holdings, Inc.* | 0.008 | 6,811.20 | 2,38,168.00 | 308 | 308 | 22.17 | 3.07 | 20.17 |

Notes:

- Source: RHP; P/E Ratio for domestic peers is based on CMP as on December 3, 2024 (NSE) & for global peers, based on CMP on NASDAQ as on December 3, 2024.

- For Affirm Holdings and One 97 Communications, P/E ratio is not ascertainable due to negative EPS.

- Conversion Rate: 1 USD = 80 INR.

- *PayPal Holdings data is for the fiscal year ending December 31, 2023.

Our Take:

- The IPO is attractively priced at P/BV of 10.06 based on its NAV of Rs. 27.74 as of June 30, 2024, and at a P/BV of 2.97 based on its post-IPO NAV of Rs. 94.05 (at the upper cap).

- MobiKwik offers a compelling investment opportunity in its IPO, backed by a robust growth strategy and a proven track record of innovation in the fintech space. The company is scaling its product portfolio across payments, credit, wealth management, and insurance, while actively launching new solutions such as soundboxes, POS machines, and Merchant Credit Advances (MCA) to drive merchant retention and recurring revenue.

- With consumer-focused offerings like “Credit on UPI,” consumer durable loans, and co-branded credit cards, MobiKwik is positioned to capture significant market demand. The revitalized payment aggregator business, Zaakpay, has shown renewed growth post-regulatory approval, handling a GMV of ₹2,000 Cr in just three months (ending June 2024).

- Operating with a technology-driven platform, the company boasts operational leverage and improved profitability, with FY2024 revenue at ₹875 Cr and a net profit of ₹14.08 Cr. Investors looking to participate in India’s burgeoning digital financial ecosystem can view this IPO as a strategic opportunity to align with a company at the forefront of innovation and growth.

- The industry has good growth opportunities lying ahead and investor with mid to long term horizon can apply for the IPO.

Disclaimer

The stocks mentioned in this article are not recommendations. Please conduct your own research and due diligence before investing. Investment in securities market are subject to market risks, read all the related documents carefully before investing. Please read the Risk Disclosure documents carefully before investing in Equity Shares, Derivatives, Mutual fund, and/or other instruments traded on the Stock Exchanges. As investments are subject to market risks and price fluctuation risk, there is no assurance or guarantee that the investment objectives shall be achieved. Lemonn (Formerly known as NU Investors Technologies Pvt. Ltd) do not guarantee any assured returns on any investments. Past performance of securities/instruments is not indicative of their future performance.