Home Loan EMI Calculator + How Banks Calculate EMI

Buying a home is one of the biggest financial decisions most people make. Before applying for a home loan, it’s important to understand how your EMI (Equated Monthly Installment) is calculated and how it impacts your monthly budget.

A Home Loan EMI Calculator helps you estimate your monthly repayment amount based on the loan amount, interest rate, and loan tenure. Understanding this calculation can help you choose the right loan and avoid financial stress later.

In this guide, we’ll explain how banks calculate EMIs, the factors that affect them, and how you can estimate your home loan payments before applying.

What Is a Home Loan EMI?

EMI stands for Equated Monthly Installment.

It is the fixed amount you pay to the bank every month until your home loan is fully repaid.

An EMI consists of:

- Principal Amount (loan amount borrowed)

- Interest Amount (charged by the lender)

During the initial years of a loan, a larger portion of the EMI goes toward interest. As the loan progresses, a greater share goes toward repaying the principal.

What Is a Home Loan EMI Calculator?

A Home Loan EMI Calculator is an online tool that helps borrowers estimate:

- Monthly EMI

- Total interest payable

- Total repayment amount

- Loan affordability

Instead of manually calculating complex formulas, you simply enter:

- Loan amount

- Interest rate

- Loan tenure

The calculator instantly displays the estimated EMI.

“Start investing with confidence! Explore

0 demat account

and grow your wealth.”

How Do Banks Calculate Home Loan EMI?

Banks use a standard mathematical formula to calculate EMIs.

EMI Formula

EMI=(1+R)N−1P×R×(1+R)N

Where:

| Symbol | Meaning |

|---|---|

| P | Loan Amount (Principal) |

| R | Monthly Interest Rate |

| N | Loan Tenure in Months |

This formula ensures that the borrower pays a fixed monthly installment throughout the loan period.

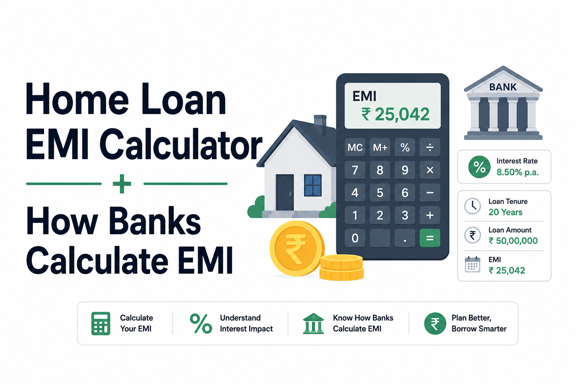

Example of EMI Calculation

Suppose:

- Loan Amount: ₹50,00,000

- Interest Rate: 8.5% per annum

- Loan Tenure: 20 years

The monthly EMI would be approximately:

₹43,391 per month

Loan Summary

| Particulars | Amount |

|---|---|

| Loan Amount | ₹50,00,000 |

| Interest Rate | 8.5% |

| Tenure | 20 Years |

| Approximate EMI | ₹43,391 |

| Total Interest Payable | ₹54+ lakh (approx.) |

| Total Repayment | ₹1.04+ crore (approx.) |

This example highlights how interest can significantly increase the total repayment amount over a long tenure.

Factors That Affect Your Home Loan EMI

Several factors influence the EMI amount.

1. Loan Amount

The higher the loan amount, the higher the EMI.

For example:

- ₹20 lakh loan = Lower EMI

- ₹80 lakh loan = Higher EMI

Borrow only what you genuinely need.

2. Interest Rate

Even a small difference in interest rates can have a major impact on long-term repayment.

Example:

- 8% interest

- 9% interest

The EMI and total interest burden can vary substantially over 20–30 years.

3. Loan Tenure

Longer tenure:

- Lower EMI

- Higher total interest

Shorter tenure:

- Higher EMI

- Lower total interest

Finding the right balance is important.

4. Type of Interest Rate

Banks generally offer:

Fixed Rate Loans

- EMI remains stable

- Predictable repayment

Floating Rate Loans

- EMI may change with market interest rates

- Can become cheaper or more expensive over time

How to Use a Home Loan EMI Calculator

Most online EMI calculators require three inputs.

Step 1: Enter Loan Amount

Example:

₹30,00,000

Step 2: Enter Interest Rate

Example:

8.75% per annum

Step 3: Enter Loan Tenure

Example:

20 years

The calculator instantly shows:

- Monthly EMI

- Total interest payable

- Total repayment amount

This helps compare different loan scenarios before applying.

Benefits of Using a Home Loan EMI Calculator

Better Financial Planning

You can determine whether the EMI fits comfortably within your monthly budget.

Compare Loan Options

Evaluate different:

- Banks

- Interest rates

- Loan tenures

Faster Decision-Making

Instant calculations save time and reduce guesswork.

Understand Total Cost

Many borrowers focus only on EMI and ignore total interest costs. A calculator reveals the complete repayment picture.

How Much EMI Can You Afford?

A common financial rule suggests that all EMIs combined should not exceed:

40% to 50% of your monthly income

Example

| Monthly Income | Recommended Maximum EMI |

|---|---|

| ₹50,000 | ₹20,000–₹25,000 |

| ₹80,000 | ₹32,000–₹40,000 |

| ₹1,00,000 | ₹40,000–₹50,000 |

| ₹1,50,000 | ₹60,000–₹75,000 |

Banks also use similar guidelines while assessing loan eligibility.

Tips to Reduce Your Home Loan EMI

Make a Higher Down Payment

A larger down payment reduces the loan amount and EMI burden.

Choose a Longer Tenure Carefully

A longer tenure lowers EMI but increases total interest paid.

Improve Your Credit Score

A higher credit score can help you qualify for better interest rates.

Make Part-Prepayments

Periodic prepayments reduce:

- Outstanding principal

- Future interest burden

- Loan tenure

Compare Multiple Lenders

Different banks and housing finance companies offer different rates and terms.

Always compare before finalizing a loan.

Common Mistakes Home Loan Borrowers Make

Focusing Only on EMI

A low EMI may result in significantly higher total interest costs.

Ignoring Processing Charges

Consider:

- Processing fees

- Legal charges

- Technical valuation fees

Borrowing Beyond Affordability

Choose a loan amount that leaves room for other financial goals.

Not Comparing Interest Rates

Even a small rate difference can save lakhs of rupees over the loan tenure.

Home Loan EMI vs Interest Cost

Many borrowers are surprised to learn how much interest accumulates over long loan tenures.

A simple illustration:

| Loan Tenure | EMI | Total Interest |

|---|---|---|

| 10 Years | Higher | Lower |

| 20 Years | Moderate | Higher |

| 30 Years | Lower | Much Higher |

Lower EMI often comes at the cost of paying more interest overall.

Key Takeaways

- EMI is the fixed monthly payment made toward a home loan.

- Banks calculate EMIs using a standard amortization formula.

- Loan amount, interest rate, and tenure directly affect EMI.

- Online EMI calculators help estimate monthly payments instantly.

- Longer tenures reduce EMI but increase total interest costs.

- Compare lenders and repayment options before taking a home loan.

- Keep your EMI within a comfortable percentage of your monthly income.

Frequently Asked Questions

Q. What is the formula used to calculate home loan EMI?

Banks use a standard EMI formula based on principal amount, monthly interest rate, and loan tenure.

Q. Does a higher tenure reduce EMI?

Yes. A longer repayment tenure lowers the monthly EMI but increases the total interest paid over the life of the loan.

Q. Is a home loan EMI calculator accurate?

Yes. Most EMI calculators provide highly accurate estimates based on the details entered. Actual figures may vary slightly depending on lender-specific charges.

Q. Can I reduce my EMI after taking a home loan?

You may reduce your EMI by refinancing, negotiating a lower interest rate, extending tenure, or making partial prepayments.

Q. What is a good EMI-to-income ratio?

Financial experts generally recommend keeping total monthly EMIs within 40–50% of your monthly income.

Conclusion

A Home Loan EMI Calculator is one of the most useful tools for prospective homebuyers. It helps you estimate monthly repayments, compare loan options, and understand the long-term cost of borrowing before making a commitment.

By understanding how banks calculate EMIs and evaluating factors such as loan amount, interest rate, and tenure, you can choose a home loan that aligns with your financial goals while keeping repayments manageable.

Disclaimer

The stocks mentioned in this article are not recommendations. Please conduct your own research and due diligence before investing. Investment in securities market are subject to market risks, read all the related documents carefully before investing. Please read the Risk Disclosure documents carefully before investing in Equity Shares, Derivatives, Mutual fund, and/or other instruments traded on the Stock Exchanges. As investments are subject to market risks and price fluctuation risk, there is no assurance or guarantee that the investment objectives shall be achieved. Lemonn (Formerly known as NU Investors Technologies Pvt. Ltd) do not guarantee any assured returns on any investments. Past performance of securities/instruments is not indicative of their future performance.

Related Posts

Download Lemonn

Download my app for share market trading, ipo investment, trading account, and all your investment needs.