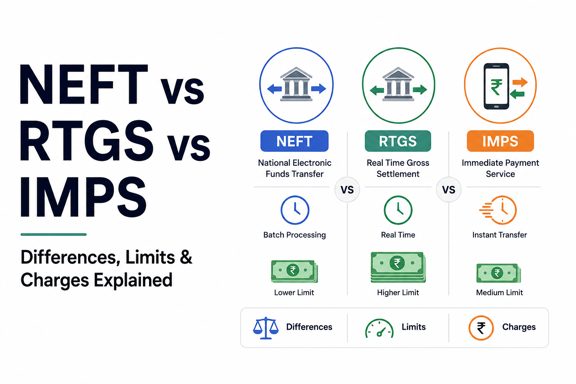

NEFT vs RTGS vs IMPS: Differences, Limits & Charges Explained

With digital banking becoming the norm, transferring money between bank accounts has never been easier. In India, three of the most commonly used fund transfer systems are NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), and IMPS (Immediate Payment Service).

While all three allow you to send money electronically, they differ in terms of processing speed, transaction limits, availability, and ideal use cases.

This guide explains the key differences between NEFT, RTGS, and IMPS so you can choose the right payment method for your needs.

Quick Comparison: NEFT vs RTGS vs IMPS

| Feature | NEFT | RTGS | IMPS |

|---|---|---|---|

| Full Form | National Electronic Funds Transfer | Real Time Gross Settlement | Immediate Payment Service |

| Transfer Speed | Usually within minutes | Instant | Instant |

| Settlement Type | Batch-wise | Real-time | Real-time |

| Availability | 24×7 | 24×7 | 24×7 |

| Minimum Amount | No minimum limit | ₹2 lakh | No minimum limit |

| Maximum Amount | Bank-specific | No upper limit (bank may set limits) | Bank-specific |

| Best For | Routine transfers | High-value transfers | Instant small to medium transfers |

| Mode | Online & Branch | Online & Branch | Online & Mobile Banking |

What Is NEFT?

NEFT (National Electronic Funds Transfer) is an electronic payment system operated by the Reserve Bank of India (RBI) that allows funds to be transferred between bank accounts across participating banks.

Earlier, NEFT transactions were processed in batches at fixed intervals. Today, NEFT is available 24×7 throughout the year.

“Start investing with confidence! Explore the

free demat account

and grow your wealth.”

Key Features of NEFT

- Available round the clock

- No minimum transfer amount

- Suitable for personal and business transactions

- Can be initiated through internet banking, mobile banking, or bank branches

- Widely accepted by almost all banks

Best Use Cases for NEFT

NEFT is ideal for:

- Paying vendors

- Sending money to family members

- Routine bank transfers

- Utility bill payments

- Education fee payments

What Is RTGS?

RTGS (Real Time Gross Settlement) is designed for high-value transactions where funds need to be transferred immediately.

In RTGS, transactions are processed individually and settled in real time, without waiting for batch processing.

Key Features of RTGS

- Instant settlement

- Primarily used for large-value transactions

- Secure and RBI-regulated

- Available 24×7 through most banks

Minimum RTGS Limit

The minimum transfer amount for RTGS is:

₹2,00,000

There is generally no RBI-imposed upper limit, although individual banks may set transaction caps.

Best Use Cases for RTGS

RTGS is suitable for:

- Property payments

- Business transactions

- Large-value fund transfers

- Urgent payments exceeding ₹2 lakh

What Is IMPS?

IMPS (Immediate Payment Service) is an instant interbank electronic fund transfer service operated by the National Payments Corporation of India (NPCI).

It allows users to transfer money instantly, even on weekends and holidays.

Key Features of IMPS

- Real-time fund transfer

- Available 24×7

- Works through mobile banking and internet banking

- Suitable for immediate payments

- Fast and convenient

Transfer Limits for IMPS

IMPS limits vary from bank to bank.

Many banks allow transfers ranging from:

- ₹1 to ₹5 lakh

- Some banks may offer higher limits

Always check your bank’s current transaction limits.

Best Use Cases for IMPS

IMPS is ideal for:

- Emergency fund transfers

- Personal payments

- Merchant payments

- Quick transfers outside banking hours

NEFT vs RTGS vs IMPS: Detailed Comparison

1. Transfer Speed

NEFT

NEFT transactions are processed continuously and are usually completed within minutes, though occasional delays may occur.

RTGS

RTGS transfers are settled instantly on an individual basis.

IMPS

IMPS provides immediate fund transfer with near-instant credit to the beneficiary account.

Winner: RTGS and IMPS

2. Transaction Limits

NEFT

- No minimum amount

- Maximum limit depends on the bank

RTGS

- Minimum amount: ₹2 lakh

- Generally no upper RBI limit

IMPS

- No minimum amount

- Maximum limit determined by the bank

Winner for High-Value Transfers: RTGS

3. Availability

All three services are available 24×7 through most banks.

This includes:

- Weekends

- Public holidays

- Bank holidays

Winner: Tie

4. Ideal Usage

| Transaction Type | Recommended Method |

|---|---|

| Small transfer | IMPS |

| Routine transfer | NEFT |

| Large-value transfer | RTGS |

| Urgent transfer | IMPS or RTGS |

| Business payment | NEFT or RTGS |

| Property purchase payment | RTGS |

5. Security

All three systems are regulated and considered highly secure.

Security measures include:

- Multi-factor authentication

- Bank-level encryption

- RBI and NPCI oversight

Winner: Tie

NEFT, RTGS, and IMPS Charges

Online Transfers

Most banks currently offer:

- NEFT: Free

- RTGS: Free

- IMPS: Usually free or nominal charges

Branch-Initiated Transactions

Some banks may charge service fees for transactions initiated at a physical branch.

Charges vary by:

- Bank

- Transaction amount

- Account type

Always verify the latest fee structure with your bank.

How to Transfer Money Using NEFT, RTGS, or IMPS

The process is similar for all three methods.

Step 1: Add Beneficiary

Provide:

- Beneficiary name

- Account number

- IFSC code

Step 2: Verify Details

Double-check:

- Account number

- IFSC code

- Beneficiary name

Step 3: Choose Transfer Method

Select:

- NEFT

- RTGS

- IMPS

based on your transfer amount and urgency.

Step 4: Enter Amount

Input the amount you wish to transfer.

Step 5: Authorize Transaction

Complete authentication using:

- OTP

- MPIN

- Transaction password

Funds are then transferred according to the selected method.

Which Is Better: NEFT, RTGS, or IMPS?

The best option depends on your specific requirement.

Choose NEFT If:

- You are making routine transfers.

- The payment is not extremely urgent.

- You want flexibility without minimum limits.

Choose RTGS If:

- You need to transfer ₹2 lakh or more.

- The payment is high value and time-sensitive.

- You require immediate settlement.

Choose IMPS If:

- You need instant transfers.

- The amount falls within your bank’s IMPS limit.

- You’re sending money via mobile banking.

Common Mistakes to Avoid

When using electronic fund transfers:

- Entering the wrong account number

- Choosing RTGS for amounts below ₹2 lakh

- Ignoring bank-specific transaction limits

- Forgetting to verify beneficiary details

- Exceeding daily transfer limits

Always review transaction details before confirming.

Key Takeaways

- NEFT, RTGS, and IMPS are secure electronic fund transfer systems.

- NEFT is best for regular transfers with no minimum amount requirement.

- RTGS is designed for high-value transfers of ₹2 lakh and above.

- IMPS provides instant transfers for smaller and medium-sized transactions.

- Most online NEFT and RTGS transactions are free of charge.

- The right option depends on transfer amount, urgency, and bank-specific limits.

Frequently Asked Questions

Q. Which is faster, NEFT or IMPS?

IMPS is generally faster because it provides immediate real-time fund transfer. NEFT transactions are also quick but may occasionally take slightly longer.

Q. Can I transfer less than ₹2 lakh through RTGS?

No. RTGS transactions require a minimum transfer amount of ₹2 lakh.

Q. Is IMPS available 24×7?

Yes. IMPS operates 24 hours a day, 7 days a week, including holidays.

Q. Are NEFT transactions free?

Most banks offer free online NEFT transactions, though branch-based transactions may attract charges.

Q. Which is safer: NEFT, RTGS, or IMPS?

All three are highly secure and regulated payment systems. The safety level is comparable when transactions are conducted through authorized banking channels.

Conclusion

NEFT, RTGS, and IMPS each serve different banking needs. NEFT is ideal for everyday transactions, RTGS is best for large-value transfers requiring immediate settlement, and IMPS excels in delivering instant payments around the clock.

Understanding the differences in speed, limits, and use cases can help you choose the most efficient and cost-effective transfer method for every transaction.

Disclaimer

The stocks mentioned in this article are not recommendations. Please conduct your own research and due diligence before investing. Investment in securities market are subject to market risks, read all the related documents carefully before investing. Please read the Risk Disclosure documents carefully before investing in Equity Shares, Derivatives, Mutual fund, and/or other instruments traded on the Stock Exchanges. As investments are subject to market risks and price fluctuation risk, there is no assurance or guarantee that the investment objectives shall be achieved. Lemonn (Formerly known as NU Investors Technologies Pvt. Ltd) do not guarantee any assured returns on any investments. Past performance of securities/instruments is not indicative of their future performance.

Related Posts

Download Lemonn

Download my app for seamless investment: investing app, etf investor app, share trading app , broking app, and demat account app—all in one!