Auto Sweep Facility in Banking: How to Make Your Idle Money Work Harder

What Is the Auto Sweep Facility?

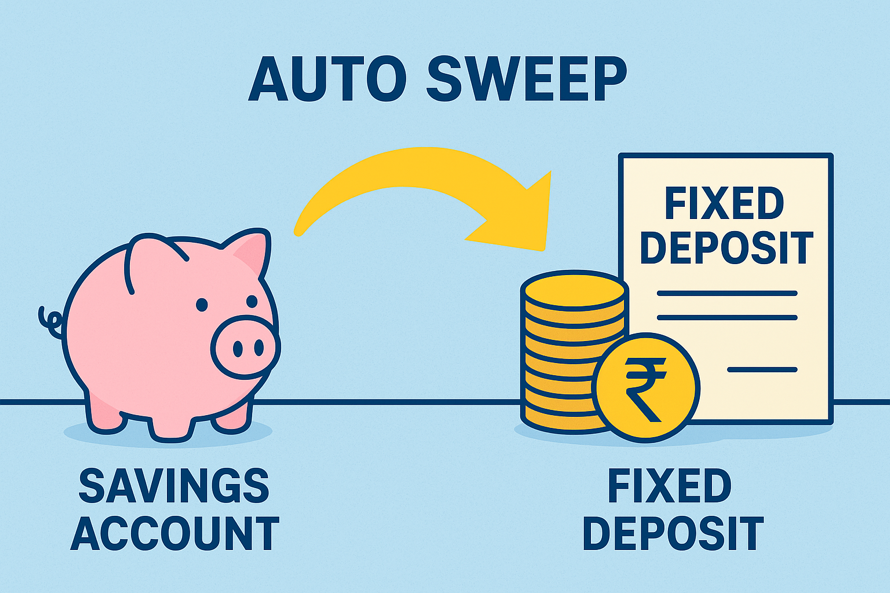

The auto sweep facility is a smart banking feature that combines the liquidity of a savings account with the higher returns of a fixed deposit (FD).

Here’s how it works:

- You set a threshold balance for your savings or current account.

- When your balance goes above this limit, the extra amount is automatically “swept out” into a linked FD.

- If your account balance drops below the limit, funds are “swept in” from the FD — no manual transfers needed.

Why Consider Auto Sweep?

Think of it as putting your lazy money to work. Instead of leaving a big chunk in your savings account earning 2–4% interest, your extra cash moves into an FD that could earn 6–8% or more — without locking it away.

“Start investing with confidence! Explore the

free demat account

and grow your wealth.”

Key Benefits:

- Higher returns on idle money — FD rates can be double or triple savings rates.

- Full liquidity — Withdraw anytime; some banks even offer zero penalty.

- Hands-off management — Everything happens automatically.

- Emergency readiness — Acts as a financial safety net without sacrificing growth.

Not All Auto Sweeps Are Equal

Different banks tweak the rules. The main differences come in:

- Premature withdrawal penalties – Some banks like Kotak Bank, IDFC FIRST Bank, and Bank of Baroda waive them. Others like SBI and ICICI charge 0.5–1%.

- Minimum sweep amounts – Can be as low as ₹1 at HDFC Bank or ₹5,000 at PNB and Axis Bank.

- FD tenure – Ranges from 46 days to 370 days or more, depending on the bank.

- Eligibility – Most residents qualify; some banks extend it to companies, HUFs, and even minors.

Potential Drawbacks to Watch For

- Taxes on interest — FD interest is taxable as per your slab.

- Minimum balance requirements — Often ₹25,000 or more.

- Complex account statements — Multiple small FDs can make tracking tricky.

- Bank-specific fine print — Especially on penalties and senior citizen interest benefits.

Best Banks for Auto Sweep in 2025

| Bank | Product Name | Penalty-Free Withdrawals? | Sweep Multiple | Typical FD Tenure |

|---|---|---|---|---|

| Kotak Bank | ActivMoney | ✅ Yes | Not fixed | Not specified |

| IDFC FIRST Bank | Auto-Sweep Savings | ✅ Yes | ₹1,000 creation / ₹1 sweep-in | 370 days |

| Bank of Baroda | Auto Sweep Facility | ✅ Yes | User-defined | User-defined |

| SBI | MODS | ❌ No | ₹1,000 | 1–5 years |

| ICICI Bank | Money Multiplier | ❌ No | ₹5,000 | 7 days–10 years |

Tips to Get the Most Out of Auto Sweep

- Set the right threshold – Keep enough for monthly expenses and emergencies.

- Pick a zero-penalty bank – If you value liquidity, avoid penalty-based banks.

- Review periodically – Adjust your threshold as your finances change.

- Track for taxes – Keep records of FD interest for filing.

Conclusion

The auto sweep facility is perfect if you maintain a healthy savings balance and want your idle money to earn more without losing access. It’s like having a high-interest savings account that adapts to your spending needs — but you need to pick the right bank and know the rules.

Used wisely, it can be the cornerstone of your emergency fund and a quiet driver of extra returns over time.

FAQs

Q. What is the auto sweep facility in banks?

The auto sweep facility is a feature where surplus money in your savings or current account is automatically transferred into a linked fixed deposit (FD) to earn higher interest. If your account balance drops below a set limit, money is automatically moved back from the FD to your account.

Q. Is auto sweep better than a savings account?

Yes, for most people who maintain a higher balance, auto sweep is better than a regular savings account because it offers FD-level interest rates on idle funds while keeping your money easily accessible.

Q. Is the interest from auto sweep taxable?

Yes. Interest earned on the FD portion of an auto sweep account is taxable according to your income tax slab. TDS may also apply if the total annual FD interest crosses the applicable limit.

Disclaimer

The stocks mentioned in this article are not recommendations. Please conduct your own research and due diligence before investing. Investment in securities market are subject to market risks, read all the related documents carefully before investing. Please read the Risk Disclosure documents carefully before investing in Equity Shares, Derivatives, Mutual fund, and/or other instruments traded on the Stock Exchanges. As investments are subject to market risks and price fluctuation risk, there is no assurance or guarantee that the investment objectives shall be achieved. Lemonn (Formerly known as NU Investors Technologies Pvt. Ltd) do not guarantee any assured returns on any investments. Past performance of securities/instruments is not indicative of their future performance.

Related Posts

Download Lemonn

Download my app for seamless investment: investing app, etf investor app, share trading app , broking app, and demat account app—all in one!