Types of GST in India: An Explainer

Imagine, for a moment, the tax maze a business faced in India before 2017: state excise, service tax, VAT, multiple registrations, cross-border transactions, and paying taxes at each step. Then, in July 2017, GST turned the page. It did not just change a rule or two; it rewrote the entire tax playbook.

Today, nearly eight years on, GST has emerged as the backbone of India’s indirect taxation architecture. It simplifies, unifies, and digital-enables. That’s the promise behind it, and for many businesses, the utility is real.

Why GST Was Introduced in India

The reason was both urgent and straightforward. India needed a common market. Goods and services crossed state borders, but every state charged differently, leading to tax-on-tax, hidden costs, and unfair competition. Businesses paid more because of complexity, not because they earned more.

GST was devised to fix that. One law, one portal, value-addition-based tax. For suppliers, this meant fewer returns. For consumers, this meant fewer surprise increases. For the economy, it meant greater fluidity.

Benefits of a Unified Tax System

Unified does not mean uniform in every detail, but it means coherent.

- Across states, similar goods attract the same slab rates, so you pay the same tax in Gujarat as you do in Assam for the same item.

- Digital invoices and input tax credits flow better. Businesses reclaim tax on what they buy, so they do not pay tax on tax.

- Compliance is faster, easier: one registration, one GST portal, one return (for many).

- Border delays drop. Logistics become smoother.

- Ultimately, consumers benefit: less hidden tax, more transparent pricing.

To sum up: GST created a framework that aligns India’s tax system with its ambition.

“Start investing with confidence! Explore

0 demat account

and grow your wealth.”

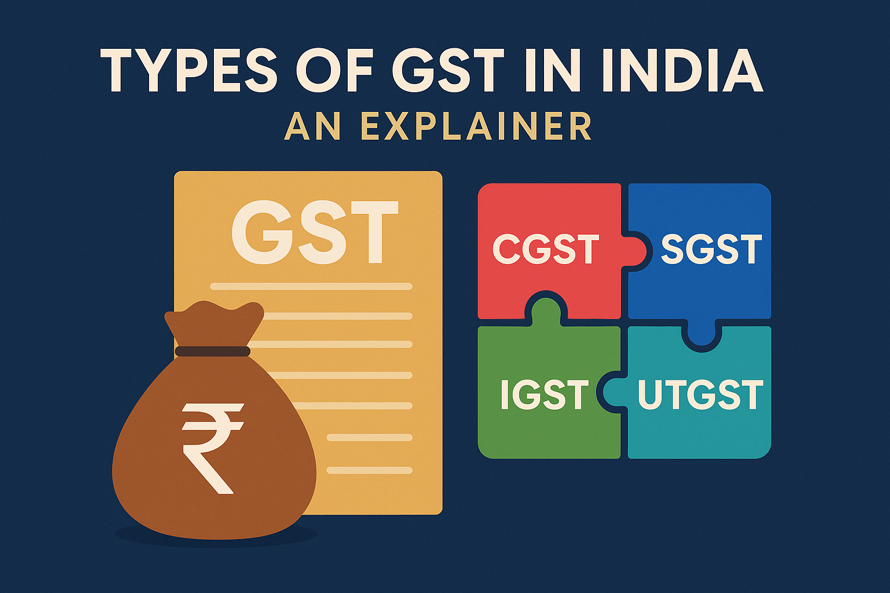

Different Types of GST in India

When you hear “GST,” you might think of one monolithic tax. In practice, India uses four main variants. The term Types of GST in India covers these: CGST, SGST, IGST, and UTGST. Each applies depending on where the supply happens and who collects the tax.

CGST – Central Goods and Services Tax

CGST is the portion collected by the Central Government for intra-state supplies. If a manufacturer in Karnataka sells to a buyer in Karnataka, CGST applies. The key: supply within the same state. The Centre’s claim rests on that.

The rate corresponds to the council-notified slab for that item. It resets if the GST Council amends it. But the structure remains: intra-state = CGST component goes to the centre.

SGST – State Goods and Services Tax

Partner to CGST in intra-state supplies is SGST, the portion for the State Government. Using the earlier example: A Karnataka manufacturer selling in Karnataka triggers SGST in addition to CGST. The State collects SGST and uses it for local governance.

Together, CGST + SGST form the total GST for intra-state supplies. That dual-split ensures both Centre and State share revenue.

IGST – Integrated Goods and Services Tax

Now, here’s the special case: supplies crossing state lines. A seller in Maharashtra ships to a buyer in Tamil Nadu. That is an inter-state supply. So the tax charged is IGST.

IGST is collected by the Centre, and then a part of it is allocated to the consuming state. This ensures destination-based tax collection. The principle? Tax follows consumption, not production.

UTGST – Union Territory Goods and Services Tax

Not all territories are equal. Some union territories lack legislatures (e.g., Lakshadweep, Andaman & Nicobar Islands). For supplies within those territories, UTGST applies alongside CGST. Example: a transaction within the Andaman and Nicobar Islands attracts CGST + UTGST.

In territories with a legislature (Delhi, Puducherry, Jammu & Kashmir), SGST applies instead. So UTGST covers those places where state-legislature-based tax doesn’t apply, but functionally it mirrors SGST for this purpose.

How Different Types of GST Work in Practice

The best way to understand GST types is to look at actual supply scenarios. When, where, and how they define whether CGST, SGST, IGST, or UTGST applies.

Intra-State Transactions (CGST + SGST)

Same state, same supply, dual tax.

Picture this: A Delhi manufacturer sells furniture to a Delhi retailer. Both parties within Delhi. The applicable GST may be 18%. That 18% divides: maybe 9% CGST + 9% SGST. The manufacturer collects both parts, remits CGST to the Central pool, and SGST to Delhi’s treasury.

Inter-State Transactions (IGST)

Now shift states. Tamil Nadu is the buyer, Maharashtra the seller. Cross-state deal. The seller charges IGST on the invoice, say 18%. The amount goes to the Centre. Later, the Centre transfers Tamil Nadu’s share out of that. Meanwhile, the buyer claims input tax credit against IGST.

This flow prevents tax leakage, ensures fairness, and keeps state boundaries from choking trade.

Union Territories and UTGST

In Union territories without a legislature, you apply CGST + UTGST. Example: A business in Dadra & Nagar Haveli & Daman & Diu supplies locally. The tax split: CGST + UTGST. For UTs with legislature, you revert to CGST + SGST.

Getting this right matters for invoices, for compliance, for vendors operating across states and UTs.

Key Differences Between CGST, SGST, IGST, and UTGST

These terms may sound familiar, but their differences are subtle and critical. Knowing them reduces errors, fines, and audit risk.

Tax Collection Authority

- CGST: collected by the Central Government.

- SGST: collected by the State Government of the supply location.

- IGST: collected by the Centre, but later shared with the consumer state.

- UTGST: collected by the Centre for the union territory without a legislature.

Applicability Based on Location

- Same supplier & buyer state → CGST + SGST.

- Supplier and buyer in different states → IGST.

- Supply within a union territory without legislature → CGST + UTGST.

- Supply involving UT with legislature → CGST + SGST (if intra-UT) or IGST (if inter-UT).

Revenue Sharing Between States and Centre

In intra-state supplies, revenue is split right at the front: Centre gets CGST, State gets SGST.

In inter-state supplies, IGST is collected centrally, then distributed: the consuming state receives its share via a settlement mechanism. This ensures the destination state, not the manufacturing state, gets the tax benefit. That shift matters when thinking of structure and fairness.

Impact of GST on Businesses and Consumers

GST reshaped more than tax bills. It changed business behavior, logistics, pricing, and transparency. For consumers and enterprises alike, it matters.

Simplified Tax Compliance

Gone are the days of separate VAT, excise, and service tax registrations. Under GST, you often have one registration, one return (especially for simpler businesses).

In 2025, thresholds matter: for e-invoicing, businesses with AATO ≥ ₹10 crore (since April 1, 2025) must upload invoices within 30 days of issue. Other thresholds remain: ₹5 crore AATO triggered e-invoice earlier. These digital reforms reduce errors and make compliance faster.

Reduced Cascading Effect of Taxes

Under the old tax structure, each stage of production added tax on the previous tax – a tax-on-tax effect. GST fixes that. Input tax credit allows a manufacturer to deduct the tax it has already paid from the tax it must pay.

Lower embedded taxes mean lower prices, or higher margins for businesses. For consumers, that often means better value.

Improved Transparency in Pricing

When you buy a product today, the invoice lists how much tax goes to the Centre, how much to the State. That clarity removes hidden costs.

Uniform slabs across states make pricing less volatile. Consumers benefit from predictability; businesses gain from clarity.

Conclusion – Understanding GST for Better Compliance

When you piece it together, the Types of GST in India fall into place like gears in a machine: CGST, SGST, IGST, UTGST, each with its role. The rules depend on where the supply happens, who consumes, and which territory is involved.

For businesses, getting this right means smoother operations, fewer penalties, and cleaner books. For consumers, it means fairer prices and simpler invoices. For India, it means a unified market with less friction.

GST is not just a tax law; it is infrastructure. And when you understand how the types work, you operate smarter, more compliant, and more confidently.

FAQs

Q1: How many types of GST are there in India?

There are four: CGST, SGST, IGST, and UTGST.

Q2: What is the difference between CGST and SGST?

Both apply for supplies within the same state. CGST is collected by the Centre; SGST by the respective State Government.

Q3: When is IGST applicable in India?

IGST is applicable when a supply of goods or services crosses state boundaries (inter-state) or involves an import or export scenario.

Q4: What is UTGST, and where is it applied?

UTGST applies in union territories without a legislature (for example, Lakshadweep, Andaman & Nicobar Islands, Dadra & Nagar Haveli & Daman & Diu). On intra-UT supplies in such territories, you would apply CGST + UTGST.

Q5: How do businesses decide which type of GST to charge?

They determine where the supplier is located, where the buyer is located, whether the supply crosses state borders, and whether the location involves a union territory with or without a legislature. Based on that, they apply either CGST + SGST/UTGST (intra-state) or IGST (inter-state).

Disclaimer

The stocks mentioned in this article are not recommendations. Please conduct your own research and due diligence before investing. Investment in securities market are subject to market risks, read all the related documents carefully before investing. Please read the Risk Disclosure documents carefully before investing in Equity Shares, Derivatives, Mutual fund, and/or other instruments traded on the Stock Exchanges. As investments are subject to market risks and price fluctuation risk, there is no assurance or guarantee that the investment objectives shall be achieved. Lemonn (Formerly known as NU Investors Technologies Pvt. Ltd) do not guarantee any assured returns on any investments. Past performance of securities/instruments is not indicative of their future performance.

Related Posts

Download Lemonn

Download my app for share market trading, ipo investment, trading account, and all your investment needs.