Hexaware Technologies Ltd – IPO Highlights

Executive Summary:

Hexaware Technologies is a global digital and technology services company focused on AI-driven solutions. It supports digital transformation and operations across six industries: Financial Services, Healthcare & Insurance, Manufacturing & Consumer, Hi-Tech & Professional Services, Banking, and Travel & Transportation. Its offerings include Design & Build, Secure & Run, Data & AI, Optimize, and Cloud Services. The company utilizes AI-enabled platforms like RapidX™, Tensai®, and Amaze® to serve clients across the Americas, Europe, Asia-Pacific, India, and the Middle East.

In this note, we take a quick look at the key highlights of the offering and deep dive into the company’s financials in comparison to its listed peers.

| Key Things to Know | |

| IPO Date | 12th Feb 2025 – 14th Feb 2025 |

| Price Band | Rs 674-708 per share |

| Total Issue Size | Rs 8,750 crores |

| Fresh Issue | – |

| Offer for Sale | Rs 8,750 crores |

| Post Issue M-cap | Rs43,025 crores at upper band |

| QIB quota | 50% |

| Retail quota | 35% |

| NII(HNI) quota | 15% |

Before we delve deeper, let’s look at the key strengths and risk factors to be considered before one decides on investing in this IPO.

Key Strengths:

- Deep Industry Expertise: Hexaware provides tailored digital transformation solutions across six industries, leveraging deep domain knowledge to address unique sub-vertical needs.

- AI-Led Innovation: The company has developed three in-house AI platforms—RapidX™ (digital transformation), Tensai® (AI automation), and Amaze® (cloud adoption)—to enhance service offerings.

- Strong Blue-Chip Clientele: Serving 31 Fortune 500 companies, Hexaware derives ~62%/83% of its revenue from clients with >$5B/>$1B revenue. Top client relationships average 15 years, with multi-year contracts.

- Global Scalable Delivery: With operations across India, UAE, USA, Mexico, Europe, and SE Asia, Hexaware offers flexible, cost-effective solutions. It prioritizes AI training, with employees earning 19,139 Gen AI certifications in 2023.

Key Risks:

- Geographic & Demand Risk: With 73.4%/71.5% of revenue from the Americas and 20.5%/22.1% from Europe (9MCY24/CY23), regional concentration and potential outsourcing budget cuts pose revenue risks.

- Talent & Operational Efficiency Risk: Business success depends on attracting skilled professionals and maintaining high employee productivity and resource utilization.

Industry Overview & Outlook:

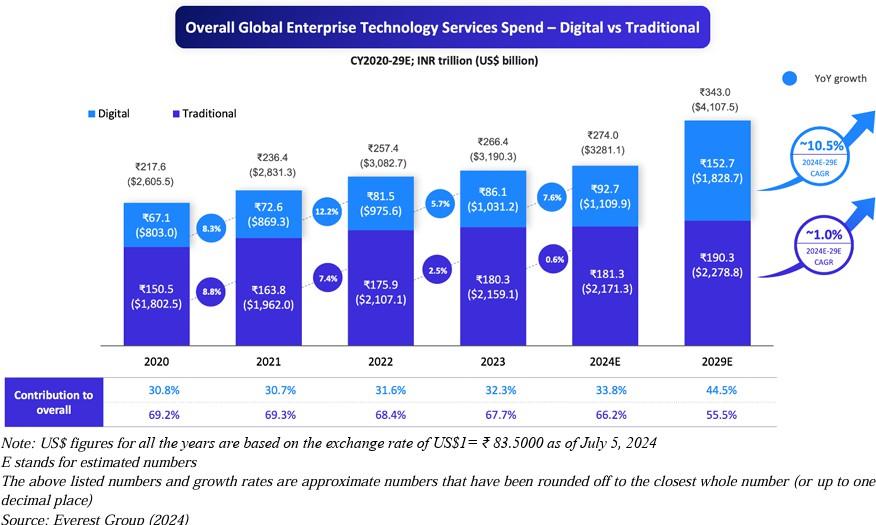

Enterprise Technology Spending: The global enterprise technology spends, covering IT services, software, and hardware, is forecasted to grow at a CAGR of 7.3% from CY2024-29E, reaching ₹630.7 trillion (US$7,552.7 billion). Digital services, driven by technologies like AI, cloud, IoT, and blockchain, are transforming business operations and customer experiences. With enterprises prioritizing innovation, digital service spending is set to outpace traditional services, growing at a CAGR of 10.5% (CY2024-29E).

Digital Transformation Acceleration: Increased enterprise spending on AI, cloud computing, automation, and data-driven solutions is driving demand for IT services.

Generative AI (Gen AI) Boom: The outsourced Gen AI services market is projected to grow at a CAGR of 60-62% (CY2024-29E), reaching ₹7.5-7.9 trillion (US$89.8-94.6 billion).

Industry-Specific Trends:

- Banking & Financial Services: 18% of global outsourced services spend (~₹14.8 trillion), driven by open banking, payments innovation, and AI-based risk management.

- Healthcare & Insurance: 24.9% of outsourced spend (~₹20.5 trillion), fueled by AI- driven diagnostics, claims automation, and compliance needs.

Challenges & Headwinds:

- Pricing and margin pressures due to cost-cutting measures.

- Growing talent shortages in AI, cloud computing, and cybersecurity.

- Increased insourcing, with 48% of enterprises favoring in-house IT services.

Peer Comparison: FY24

| Particulars (Rs cr) | Hexaware Technologies Ltd. | Persistent Systems Ltd. | Coforge Ltd. | LTlMindtree Ltd. | Mphasis Ltd. |

| CMP | 708 | 5,828.40 | 8,096.80 | 5,677.70 | 2,713.60 |

| Sales | 10,380.30 | 9,822.00 | 9,179.00 | 35,517.00 | 13,932.00 |

| EBITDA | 1,581.10 | 1,676.00 | 1,428.00 | 6,387.00 | 2,422.00 |

| Net Profit | 997.6 | 1,093.00 | 836 | 4,585.00 | 1,555.00 |

| Mkt Cap. | 43,024.80 | 89,543.30 | 50,007.80 | 1,72,967.60 | 51,687.40 |

| EBITDA Margin (%) | 15.2 | 17.1 | 15.6 | 18 | 17.4 |

| Net Margin (%) | 9.6 | 11.1 | 9.1 | 12.9 | 11.2 |

| PE (x) | 43.1 | 88.3 | 68.2 | 38.4 | 34.5 |

| EV/EBITDA (x) | 26.4 | 57.1 | 40 | 27.1 | 22.5 |

| ROE (%) | 22.8 | 24 | 24.1 | 25 | 18.4 |

| ROCE (%) | 29.6 | 29.2 | 28.6 | 31.2 | 24 |

Our Take: Slight valuation discount to peers

At the upper price band, Hexaware trades at 43x CY23 P/E, slightly at a discount compared to its peers. The company enjoys a diversified revenue mix and uses AI to enhance productivity and utilization. Revenue (INR) and PAT grew at a CAGR of 20%/15% (CY21-23) with stable EBIT margins. Investors with long-term horizon can consider subscribing.

Key Financials:

| Particulars (Rs cr) | CY21 | CY22 | CY23 | GMCY24 |

| Revenue from operations | 7,178 | 9,200 | 10,380 | 8,820 |

| EBITDA | 1,133 | 1,222 | 1,581 | 1,340 |

| EBIT | 908.8 | 977.3 | 1297.5 | 1137.3 |

| PAT | 748.8 | 884.2 | 997.6 | 857.5 |

| EBITDA Margin (%) | 15.8 | 13.3 | 15.2 | 15.2 |

| EBIT Margin (%) | 12.7 | 10.6 | 12.5 | 12.9 |

| PAT Margin (%) | 10.4 | 9.6 | 9.6 | 9.7 |

| ROE (%) | 19.8 | 22.4 | 22.8 | |

| ROCE (%) | 25.8 | 28.9 | 29.6 |

Disclaimer

The stocks mentioned in this article are not recommendations. Please conduct your own research and due diligence before investing. Investment in securities market are subject to market risks, read all the related documents carefully before investing. Please read the Risk Disclosure documents carefully before investing in Equity Shares, Derivatives, Mutual fund, and/or other instruments traded on the Stock Exchanges. As investments are subject to market risks and price fluctuation risk, there is no assurance or guarantee that the investment objectives shall be achieved. Lemonn (Formerly known as NU Investors Technologies Pvt. Ltd) do not guarantee any assured returns on any investments. Past performance of securities/instruments is not indicative of their future performance.